Bending Spoons IPO: What Happens to Evernote Features, Pricing, and User Data When a Profit-Optimizing Roll-Up Goes Public

Bending Spoons' IPO introduces structural incentives that will likely accelerate monetization of Evernote through further price increases, AI-feature gating, and storage-limit tightening, while reducing the likelihood of non-monetizable feature investment. This article analyzes what the S-1/F-1 filing reveals about Evernote's future for current subscribers.

Category: Note-Taking App

Pricing model: Freemium

Free plan: Yes

Best for: Knowledge Workers

Pricing last verified: 2026-04-09

- Evernote

- vendor-risk

- pricing-change

- note-taking

- data-portability

The Bending Spoons Playbook: Acquire, Gut, Raise Prices, Repeat

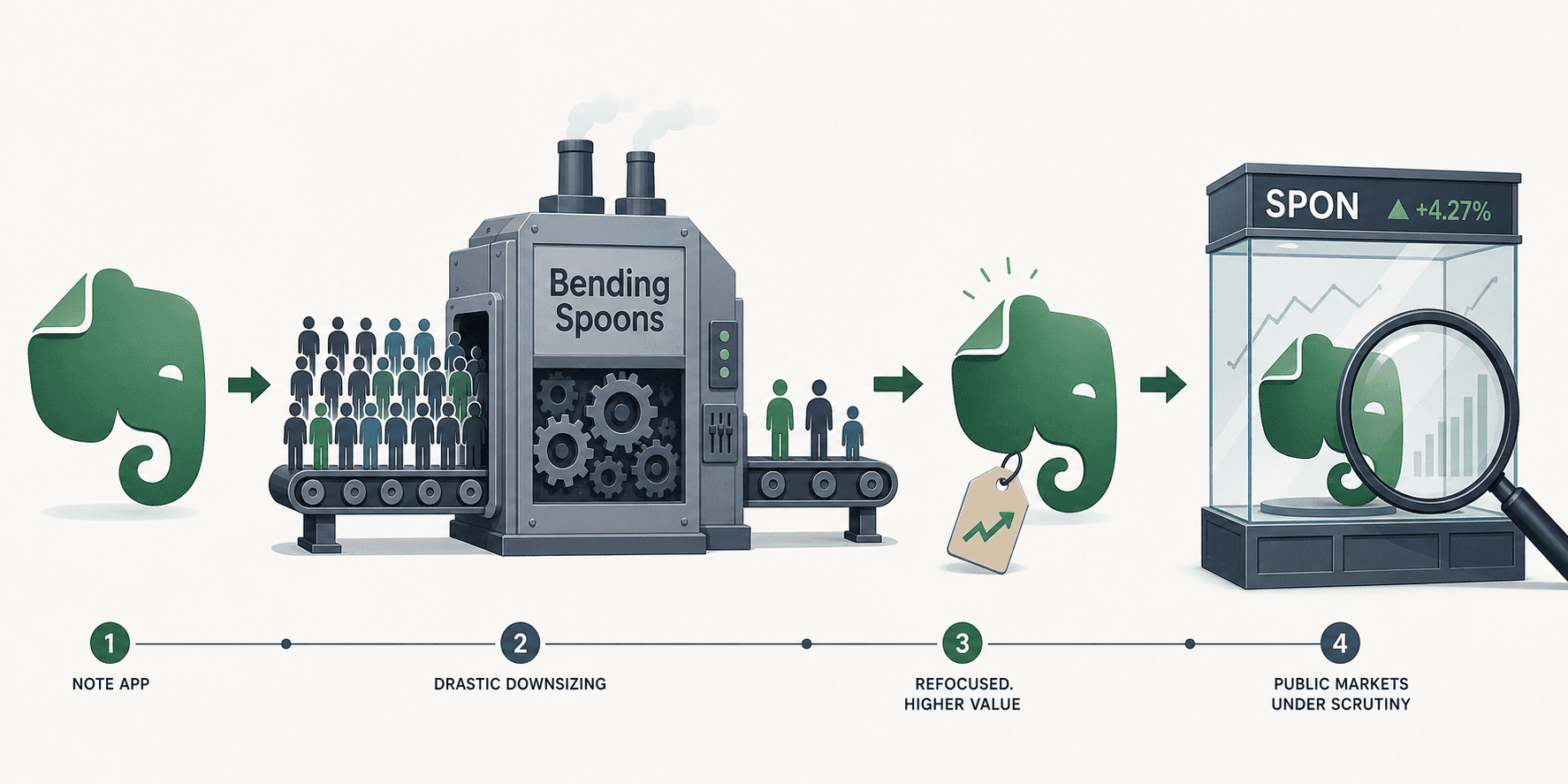

Bending Spoons did not acquire Evernote in late 2022 to nurture it. The company's track record, now documented across more than 50 acquisitions, follows a repeatable pattern: buy a once-dominant consumer app with a loyal user base, slash operating costs, accelerate product releases, and raise prices aggressively. Evernote is the clearest proof case of this strategy in action.

When Bending Spoons took over, Evernote employed 341 people. Within months, that number dropped to approximately 60 — an 82% reduction in headcount. Management layers collapsed from four to two. The monolithic codebase was broken into microservices. Product releases, which had been sluggish for years, jumped 50% in 2023 and then doubled in 2024.

The cost-cutting was brutal but effective by the numbers. The revenue side of the equation, however, tells a different story. According to Appfigures estimates, Evernote's monthly net revenue averaged about $1.5 million in the six months before the acquisition, with roughly 254,000 monthly downloads. In the most recent six-month period, revenue climbed to an average of $2.1 million per month — a 39% increase — while downloads collapsed to about 92,000 per month, a decline of 64%.

- Staff reduced from 341 to ~60 (82% cut)

- Management flattened from 4 layers to 2

- Product releases doubled between 2023 and 2024

- Downloads down 64%, but revenue up 39%

- Pricing has roughly tripled since acquisition

- Storage limits introduced for the first time in Evernote's history (November 2025)

The user response to these changes has been severe. Evernote's recent average star rating on app stores sits at 1.34 out of 5, with approximately 80% of recent reviews being one-star ratings. The product is more profitable than ever, but it is also more hated than ever. That tension — between profitability and user satisfaction — is the central dynamic that Bending Spoons' IPO will amplify.

The IPO Math: $20B Valuation on $1.31B Revenue with $4.36B in Debt

On June 8, 2026, Bending Spoons filed its F-1 registration statement with the SEC for a U.S. IPO on the Nasdaq under the ticker BSP. The filing reveals a company that has grown spectacularly — but almost entirely through acquisition, not organic product development. Understanding the financial structure of this IPO is essential for any Evernote user trying to predict what happens next.

The headline numbers are striking. Revenue grew 95% year over year to $1.31 billion in 2025, more than tripling between 2023 and 2025. Operating profit more than doubled to $278 million. Monthly active users reached 500 million in March 2026, up from 111 million in December 2023. Monthly paying customers tripled to 9 million over the same period.

But beneath the top-line growth, the balance sheet tells a more precarious story.

| Metric | Value | Significance for Evernote Users |

|---|---|---|

| IPO valuation target | $20 billion (reported market speculation) | Creates pressure to demonstrate sustained growth to justify the multiple |

| 2025 revenue | $1.31 billion | 95% YoY growth, but 82% of that growth came from acquisitions |

| Total debt | $4.36 billion | Debt service competes with product investment for cash |

| 2025 interest expense | $143 million | Grew 337% year over year; consumes cash that could fund development |

| Q1 2026 interest expense | $93 million | Consumed 78% of Q1 2026 operating income |

| Q1 2026 reorganization costs | $76 million | Restructuring is ongoing, not finished |

| Organic revenue growth (2025) | 13% | Only 13 of 95 percentage points of growth came from existing products |

| GAAP net income (2025) | -$0.2 million | On a GAAP basis, the company barely broke even |

| Adjusted Net Income (2025) | $376 million | Adjusted figures exclude $151M in amortization and impairment, $85M in transaction costs, and $79M in reorganization expenses |

The debt burden is the most important number for Evernote users to understand. Bending Spoons carries $4.36 billion in total debt against $741 million in cash. Interest expense in 2025 was $143 million, growing 337% year over year. In Q1 2026 alone, interest expense reached $93 million — consuming 78% of that quarter's operating income. When a company spends more than three-quarters of its operating profit on interest payments, every dollar of revenue from every product becomes critical.

This is the structural reality that will shape Evernote's future. Bending Spoons cannot afford to let any of its revenue-generating assets underperform. And the easiest way to increase revenue from a sticky product with a 99% net revenue retention rate is to raise prices.

What the S-1 Reveals About Evernote: Revenue Growth Through Price Hikes

The F-1 filing does not break out Evernote's individual financial performance, but the aggregate data combined with Appfigures estimates paints a clear picture: Evernote is being monetized through price increases, not user growth or feature innovation.

Pricing has roughly tripled since Bending Spoons took over. The new plan structure, introduced in late 2025 and finalized in April 2026, eliminated the legacy Personal and Professional tiers entirely. Existing users were migrated to either Starter at $99 per year or Advanced at $249.99 per year. In some regions, the Advanced plan represents a 101% price increase over the previous Professional plan.

| Plan | Annual Price | Key Limits | Notes |

|---|---|---|---|

| Starter | $99/year | 1,000 notes, 20 notebooks, 1,000 attachments, 5 GB storage, 3 synced devices | Replaces Personal plan at significantly higher price |

| Advanced | $249.99/year | Unlimited notes, notebooks, attachments, storage, and devices | 101% increase over Professional in some regions |

| Legacy Personal/Professional | Discontinued | N/A | Cannot be reverted to once migrated |

The introduction of storage limits in November 2025 was a watershed moment. For the first time in Evernote's history, power users faced a hard cap on storage unless they paid for the Advanced tier. This is a textbook Bending Spoons move: create a pain point, then offer the premium tier as the solution. The 5 GB limit on Starter is deliberately tight for anyone who uses Evernote for document storage, PDF annotation, or image-heavy notes.

The most telling metric in the F-1 filing is Net Revenue Retention (NRR) by asset. Evernote has the highest NRR in Bending Spoons' portfolio at 99%. For context, StreamYard sits at 91% and Remini at 87%. A 99% NRR means that for every $100 Evernote earned from existing subscribers last year, it earned $99 again this year — before any new sales or price increases. That stickiness makes Evernote the most valuable asset for monetization experiments.

The math is straightforward. If Bending Spoons needs to demonstrate accelerating revenue growth to public-market investors — and it does, given the debt burden and the 18x revenue multiple implied by a $20 billion valuation — the path of least resistance is to raise prices on the product with the highest retention rate. New features, especially non-monetizable ones like bug fixes, performance improvements, or UX refinements, do not move the revenue needle. Price increases do.

How Public-Company Pressure Changes Incentives for Evernote Users

The shift from private to public ownership is not just a financial event — it is a structural change in how decisions are made. Private companies can optimize for long-term user satisfaction, product quality, and sustainable growth. Public companies must optimize for quarterly earnings expectations. For a company carrying $4.36 billion in debt with interest costs consuming 78% of operating income, the quarterly pressure is extreme.

Here is how that pressure will likely translate into product decisions for Evernote:

- Faster monetization of existing features. Any capability that can be moved from the Starter tier to the Advanced tier will be. Storage limits were the first example; AI features, offline access, or advanced search could be next.

- AI features as upsell hooks, not genuine improvements. Semantic Search, currently in beta for Advanced and Enterprise users, is positioned as a premium differentiator. If it drives upgrades from Starter to Advanced, it will be considered a success — regardless of whether it meaningfully improves the note-taking experience.

- Reduced investment in non-monetizable features. Bug fixes, accessibility improvements, performance optimization for large archives, and UX refinements do not appear on earnings calls. Expect the pace of these improvements to slow as engineering resources are directed toward monetizable features.

- More aggressive tiering. The two-tier structure (Starter and Advanced) could easily become three or four tiers, with features stripped from lower tiers and added to higher ones. This is the standard SaaS playbook for driving upgrades.

- Less responsiveness to user feedback. When the primary customer is the public market, not the end user, product decisions are driven by revenue metrics rather than user satisfaction scores. The 1.34-star rating is already being tolerated because revenue is up 39%.

The contrast between pre-IPO and post-IPO incentives is stark. Before the IPO, Bending Spoons could afford to make long-term bets — the 82% staff reduction and codebase modernization were painful but positioned the product for future efficiency. After the IPO, the company must meet quarterly expectations with a portfolio that has only 13% organic growth. The easiest lever to pull is the one that has already worked: raise prices on the stickiest asset.

User Data Risk: Material Weaknesses in Accounting Controls and What They Mean

One of the most concerning disclosures in the F-1 filing has nothing to do with pricing or features. Bending Spoons explicitly acknowledges "material weaknesses" in its internal controls over financial reporting. The filing cites: absence of clearly defined structures and accountability, limited SEC reporting experience, insufficient SOX and GAAP expertise, lack of segregation of duties, and weak controls over journal entries across all financial statements.

This is a governance red flag. Material weaknesses in financial controls mean that the company's own auditors have identified a reasonable possibility that a material misstatement of financial reports could occur and not be prevented or detected. For a company that processes subscription payments for 9 million paying customers and stores personal data for 500 million monthly active users, weak financial controls raise questions about the broader control environment — including data governance and privacy compliance.

The data risk becomes more acute when you consider what could happen if Bending Spoons needs to sell assets to service its $4.36 billion debt. The F-1 filing shows $76 million in reorganization costs in Q1 2026 alone — restructuring is ongoing, not finished. If Evernote's revenue growth slows or if the company needs to raise cash quickly, the note archive of every Evernote user becomes an asset that could be sold, licensed, or used in ways that current privacy policies do not anticipate.

Semantic Search, Evernote's flagship AI feature, uses the company's "internal AI models" to index and retrieve user notes. This means your note content is being processed by Evernote's servers for AI training and inference. Under a public company with weak controls and debt pressure, the question of how that data is protected, who has access to it, and whether it could be monetized in ways not currently disclosed becomes a real concern.

The S-1/F-1 filing discloses 'material weaknesses' in accounting controls: absence of clearly defined structures and accountability, limited SEC reporting experience, insufficient SOX and GAAP expertise, lack of segregation of duties, and weak controls over journal entries across all financial statements.

Historical Precedent: What Happened to AOL, Eventbrite, and Vimeo After Acquisition

Bending Spoons' playbook is not theoretical. The same pattern applied to Evernote has been applied to every major acquisition in the portfolio. Understanding what happened to other products provides a reliable forecast for Evernote's trajectory.

- AOL: Once a dominant internet portal, AOL was acquired by Bending Spoons and subjected to the same cost-cutting and monetization strategy. The brand still exists but operates as a revenue extraction vehicle rather than a growing product.

- Eventbrite: The event management platform was acquired and restructured. Staff reductions, pricing changes, and a shift toward higher-margin revenue followed. The product continues to operate but with a narrower feature set and higher costs for organizers.

- Vimeo: The video platform was acquired as part of Bending Spoons' roll-up strategy. Pricing was restructured, free tier capabilities were reduced, and the product was repositioned for higher revenue per user rather than broader adoption.

- Remini: Bending Spoons' first acquisition (mid-2021) is the portfolio's success story. By January 2026, Remini earned $7.5 million in net revenue — more than 10 times what it was making in early 2022. The pattern: aggressive monetization of a photo-enhancement app with a loyal but price-sensitive user base.

The common thread across all these acquisitions is that Bending Spoons does not build products for users who want low prices, generous free tiers, or extensive feature sets. It builds products for investors who want growing revenue and expanding margins. Every product in the portfolio is a cash flow asset, not a mission-driven platform.

What Evernote Users Should Watch For Post-IPO

The IPO does not change Evernote overnight. But it creates a set of structural incentives that will play out over the next 12 to 24 months. Here is what current subscribers should monitor as leading indicators of where the product is heading.

- Further price increases on existing plans. The most predictable outcome. If Bending Spoons needs to show revenue growth in its first few quarterly earnings reports as a public company, raising Evernote prices is the fastest lever. Watch for mid-cycle price adjustments, not just annual renewal increases.

- Free tier compression. The current free tier is already limited. Post-IPO, expect further restrictions on device limits, storage, or feature access to drive free users toward paid plans.

- Feature extraction and paywalling. Features that were previously included in lower tiers — offline access, advanced search, PDF annotation, email forwarding — may be moved to higher tiers or introduced as paid add-ons.

- Reduced responsiveness to user feedback. The 1.34-star rating and 80% one-star review rate have not changed Bending Spoons' strategy. Post-IPO, the company's primary accountability is to shareholders, not users. Do not expect feature requests or bug reports to receive the same attention.

- Potential resale of Evernote. If Evernote does not hit growth targets, or if Bending Spoons needs to raise cash to service debt, the product could be sold to another acquirer. Each sale introduces new uncertainty about data handling, pricing, and product direction.

- Changes to data privacy and AI training policies. As Semantic Search expands and Evernote's AI models evolve, watch for updates to privacy policies that expand the scope of how user note content can be used for training or monetization.

This is not a prediction that Evernote will shut down or become unusable. The product will continue to function, and for many users, the core note-taking experience will remain adequate. But the structural incentives created by the IPO point in one clear direction: the cost of using Evernote will continue to rise, the value proposition for free and lower-tier users will continue to narrow, and the product roadmap will be driven by revenue targets rather than user needs.

For users who want to understand their options, the Evernote Starter vs. Advanced plan comparison provides a detailed breakdown of what each tier actually delivers. For those considering a move, the guide to what went wrong and where to move your notes covers the migration landscape. And for a broader view of how the note-taking market is shifting, our 2026 market analysis explains why the old buying advice no longer applies.

Comments

Join the discussion with an anonymous comment.